Applying for a business credit card is easier than it sounds. Here is how to apply for one, whether you have a corporation or a freelance side hustle.

A business credit card is a great way to get extra rewards and perks.

But not all cards are created equal.

Read on for everything to know about how to apply for a business credit card.

For new businesses and first-time applicants, here are some things to know about getting approved.

For new businesses and first-time applicants, here are some things to know about getting approved.

Every business credit card is different and there are some better suited for certain types of entrepreneurs than others. When you’re shopping around for a card, keep your eyes on these four things:

Rebecca Lake is a journalist at CreditDonkey, a credit card comparison and reviews website. Write to Rebecca Lake at rebecca@creditdonkey.com. Follow us on Twitter and Facebook for our latest posts.

Note: This website is made possible through financial relationships with some of the products and services mentioned on this site. We may receive compensation if you shop through links in our content. You do not have to use our links, but you help support CreditDonkey if you do.

Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. This site may be compensated through the Advertiser’s affiliate programs.

Editorial Note: This content is not provided by Chase. Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Chase. This site may be compensated through the Advertiser’s affiliate programs.

Read Next:

- Who Can Apply?

- What You Need to Apply

- Getting Approved

- How to Compare Cards

- Frequently Asked Questions

Here are 5 steps to qualify for a business credit card:

- Have a small business with the intent to make a profit.

- Know your credit score so you know which cards you qualify for.

- Compare business credit card offers to find the best one for you.

- Fill out application with your business name and EIN (or your name and SSN).

- Wait for approval. Or call for reconsideration if rejected.

Tip: As a small business owner, you know that credit cards can be a lifesaver. But it’s not always easy to know where to start when it comes to applying for a business credit card. You’ve probably heard that getting a business credit card is important, but you don’t want to get taken advantage of by high interest rates or unfair fees.

Consider this: Ink Business Cash lets you earn $350 when you spend $3,000 on purchases in the first three months and an additional $400 when you spend $6,000 on purchases in the first six months after account opening. Earn 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet, cable and phone services each account anniversary year. Earn 2% cash back on the first $25,000 spent in combined purchases at gas stations and restaurants each account anniversary year. Earn 1% cash back on all other card purchases. There is no annual fee.

Plus, there is a 0% introductory APR on purchases for 12 months. After the intro period, a variable APR applies, currently 17.99% – 25.99%.

Who Can Apply?

Business cards aren’t just for corporations. You can apply for a business card even if you’re running a one-man show and have no office. You may be surprised by what could be considered a business. Here are just some examples:- If you’re a freelance web designer

- If you have an Etsy shop

- If you sell books on Ebay

- If you drive Uber in your spare time

- If you tutor students

- If you sell cookies at the farmer’s market

- Keep your business expenses separated. This will make it so much easier come tax time.

- Earn rewards in business categories. Besides the tempting bonuses, business credit cards generally give bonus cash back or points in popular business categories (such as office supply stores, advertising online, telecommunication services, etc.)

Ink Business Cash® Credit Card

Earn 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet, cable and phone services each account anniversary year. Earn 2% cash back on the first $25,000 spent in combined purchases at gas stations and restaurants each account anniversary year. Earn 1% cash back on all other purchases. - More purchasing power. Having a separate business credit card will mean that you have more credit for business expenses. Also, business credit cards tend to give higher credit lines than personal cards.

What You Need to Apply

Here comes the fun part: Applying for a business credit card when you’re just starting out can make you feel more official. It’s a little different than applying for a personal credit card. Here’s a rundown of how to fill out the application:- The business’ legal name

This is the name you use to do business. It’s what will show up on your card if you’re approved.If you have a corporation or an LLC, enter the business name that you registered with your state government.If you’re a freelancer or sole proprietor, just use your legal name on this line.

Tip: Small business can also file a “Doing Business As” or DBA. This allows you to operate under another business name (instead of your own name). If you have done this, apply with your DBA name.

- Your tax identification number You’ll need a tax identification number to process your application.Incorporated businesses and partnerships enter their federal Employer Identification Number. This is a nine-digit number issued by the IRS for tax reporting purposes.If you’re a freelancer, you’d enter your Social Security number on this line (unless you have an IRS-issued Employer Identification Number).

- The business type or business structure

This is the kind of business you’re operating. If you’re an LLC, you’d choose partnership or corporation, based on how it’s set up. If you are a freelancer, you would usually put down sole proprietorship.

Beneficial owners: Effective May 11, 2018, new regulations require that important personal information is also provided for beneficial owners. This is anyone who directly or indirectly owns 25 percent or more of the business. This includes names, birth dates, social security numbers, home addresses and percent of ownership. Their credit information is not pulled, but records are kept for informational purposes.[1]

- The industry type or nature of the business

Credit card companies also want to know what kind of business you’re running. You’ll have a list of industries to choose from. Just select the one that fits best, even if it isn’t quite the exact label.

Related: Successful People Do These 23 Things Daily

- Your role in the business

Spell out what you do. For example, you can say you’re the owner, president, or general manager.

Related: CEO Statistics

- Business address and phone number You’ll need to fill in the contact information for your business. If you run your business from home, just use your home address here.

- How long you’ve been in business

Enter the number of years you’ve been in business. If you’re still in the early startup phase, just enter “0” in this box.

Related: Startup Failure Rate Statistics

- The number of employees Enter the number of employees you have, if any. If it’s just you, enter “1” for yourself.

- Annual business revenue

You have to let the credit card company in on how much revenue your business is bringing in each year. If your business is new and you haven’t made a buck yet, it’s fine to put “0.”

Related: How to Make Customers Happy

- Estimated monthly spend

This just means your most accurate guess of what you think you’ll charge to the card each month. Not all business card applications ask for this, but you should be ready with an answer if it comes up. Make sure this is what you will charge for business expenses, not personal.Aside from your business information, you’ll need to connect the dots on your own personal details. That means filling in:

- Your name

- Address, phone number and email

- Social Security number

- Birth date

- Mother’s maiden name

- Household income

Getting Approved for a Business Credit Card

|

Earn $350 when you spend $3,000 on purchases in the first three months and an additional $400 when you spend $6,000 on purchases in the first six months after account opening

- It is dependent on your personal credit. Since you don’t have any business history yet, the banks will look at your personal credit history and score. The better your personal credit score is, the easier it is to qualify.

What’s your credit score?That won’t come into play as much for an established business, since you would have a separate business credit history built up.Getting a business card with bad credit: Owners with low (or no) credit can still get a business credit card but options are limited. Companies like Capital One offer cards to people with lower credit scores. They will check your personal credit score, however. You might also consider a secured credit card. These cards have lower credit requirements but require a deposit in case you default on payments. A prepaid card is a viable option and doesn’t require a credit score check, but it does not help you build credit.

- You probably need to sign a personal guarantee. This is a clause that states you’re personally responsible for the repayment of business debt. Banks often need this assurance that someone will be responsible. If you stop making payments on the card because the business fails, the bank can come after you personally to recover the balance owed.

- Do not lie on the application. Even if you need to put “0” as the revenue, it’s better to do that than lie. You may get a phone call asking for more information. Be prepared for questions about the nature of your business and how much you expect to make.Just tell the truth that you’re in the startup phase. Explain why you want the business card now. For example, maybe the reward structure will really help you, and you want to keep expenses separate.

- A relationship with the bank helps. If you’re already a customer with the bank and your accounts are in good standing, it may make it easier to apply for a business card with the same bank.

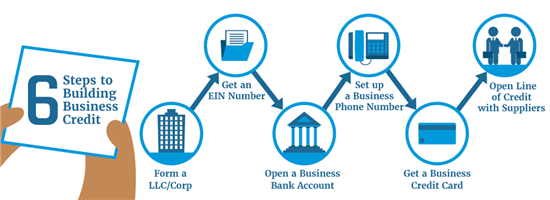

How do you obtain business credit? Here are simple steps to build business credit history:

- Form an LLC or incorporate to help separate your personal credit from that of your company.

- Apply for an EIN number. (This number will represent your business in tax filings and legal documents).

- Start a business bank account. Make sure to keep your personal financial business separate from this account.

- Apply for a business credit card. This will help you grow a line of credit for your new company.

- Pay all bills and invoices on time to build your credit history and reputation with vendors.

How to Compare Cards

|

- APR: The APR, or annual percentage rate, determines the amount of interest you’ll pay over the course of a year if you carry a balance. Many business cards offer a 0% introductory rate on purchases for new card members, which can give your new business some breathing room.

- Fees: Scoring a card with a low APR isn’t such a sweet deal if it comes with lots of fees. If your goal is earning rewards, for example, make sure they’re not being wiped out by a high annual fee. If you travel, steer clear of cards that charge a foreign transaction fee. This fee can add up to 3% to the cost of purchases made abroad.

- Rewards: Earning big rewards is one of the best reasons to get a business credit card. Choose a card with a rewards structure that aligns with your business expenses. Think about whether you want points, miles or cash back; and whether you want bonus categories or a flat rate per dollar. Also, consider your redemption options. If you’re after a big bonus, make sure you can meet the minimum spending requirement.

What is the best small business credit card? Ink Business Preferred lets you earn 90k bonus points after you spend $8,000 on purchases in the first 3 months from account opening. That’s $900 cash back or $1,125 toward travel when redeemed through Chase Travel℠. Earn 3 points per $1 on the first $150,000 spent in combined purchases on travel, shipping purchases, Internet, cable and phone services, advertising purchases made with social media sites and search engines each account anniversary year. Earn 1 point per $1 on all other purchases. There are no foreign transaction fees. There is a $95 annual fee.

- Card type: Business credit cards will allow you to carry a balance, but charge cards require you to pay in full each month. Charge cards don’t charge interest but there’s no flexibility if you need to pay just the minimum one month. If you don’t have a steady cash flow, you need to have a revolving credit card account instead.

Frequently Asked Questions

- Can I apply for business credit card even if I’m not yet earning income? Yes. You can apply as long as you have a reasonable intention to make a profit.

- I really like the rewards on a certain business card. Can I use it for personal expenses too?

We advise that you don’t mix personal and business expenses. It’ll cause more headache when you need to separate out your business expenses when filing taxes.And if you fall behind on your payments, the card issuer may look at your activities more closely. If they see that there are personal expenses on there, you may lose your rewards and your account could be closed or changed to a personal card.

Note: If you operate as an LLC, corporation, or partnership, then it’s even more important to keep your business separate from your personal life. At this point, there are legal considerations too. If you mix personal and business spending on a credit card, then the business and the person can be seen as the same. That may expose you to additional liabilities.

- Do I have to also have a business checking account in order to have a business credit card? If you’re an independent freelancer or have other small jobs (in other words, if you’re a sole proprietor), then no, you do not usually need to have a business checking account.If you have formed an LLC, partnership, or DBA (Doing Business As), then you do need a separate business banking account. These kinds of business require that you separate business and personal finances.

- Will a business credit card affect my personal credit? Generally, business credit cards don’t report to personal credit bureaus. So your personal credit won’t be impacted if you have high business expenses. However, if you keep on making late payments or missing them, then your personal credit may take a ding.

What the Experts Say

CreditDonkey asked a panel of industry experts to answer readers’ most pressing questions. Here’s what they said:

What tips do you have for keeping business and personal finances separate?

Dan Brosman

Associate Director of the Small Business Development Center at the University of Wisconsin, Oshkosh

The best way to separate your business and personal assets is by forming a legal business entity, such as an LLC, S Corp, or C Corp. An LLC is … (Continue reading)

How can using a business credit card responsibly help you build a good business credit score?

Dr. Brandon Di Paolo Harrison

Assistant Professor of Accounting at Austin Peay State University

A small business can use a business credit card to establish/improve a business’ credit rating. The business should make on-time payments, … (Continue reading)

Dr. Brandon Di Paolo Harrison

Assistant Professor of Accounting at Austin Peay State University

A small business can use a business credit card to establish/improve a business’ credit rating. The business should make on-time payments, … (Continue reading)

Is it a good idea to use a business credit card for personal expenses?

Dr. Danielle Zanzalari

Assistant Professor of Economics, Seton Hall University

It is best to keep your personal expenses separate than your business expenses. The main reason for this is most business expenses are tax … (Continue reading)

Bottom Line

In short, you can apply for a business card as long as you are earning profit (or intend to). There are plenty of incentives for choosing a business credit card over a personal credit card. You can keep your personal and business expenses separate, and you may be able to get higher rewards for your business-related charges. However, once you get it, use the card responsibly and abide by the cardholder agreement.

|

|||||||||||||||

References

- ^ FinCEN.gov. Information on Complying with the Customer Due Diligence (CDD) Final Rule, Retrieved 11/28/2022

|

|||||||||||||||

|

|

|

||||||

|

|

|

What’s your credit score?

5% Excellent (800-850)

7% Very good (740-799)

16% Good (670-739)

40% Fair (580-669)

31% Poor (300-579)

Best Small Business Bank

Discover the top 10 banks for small businesses. Unlock your business’ potential with the best bank

How to Build Business Credit

Read more about Business

A good business credit score can increase a company’s value and protect personal credit. But how can I build my business credit fast? Read on for the answer.

As a small business owner, the lines between your personal and business life can become blurred. Creating a separate business credit profile will protect your personal assets and give your business more lending power.

Building business credit is not as straightforward as building personal credit. But don’t worry, it’s not too complicated. There are just some extra steps.

We’ll go over everything you need to know.

Write to Kim Shackleton at feedback@creditdonkey.com. Follow us on Twitter and Facebook for our latest posts.

Note: This website is made possible through financial relationships with some of the products and services mentioned on this site. We may receive compensation if you shop through links in our content. You do not have to use our links, but you help support CreditDonkey if you do.

Read Next:

|

Here are 8 smart steps to establish business credit:

What is Business Credit and Why Do I Need It

Business credit is similar to personal credit, but it’s based on your business’s financial history. It’s tied to your Employer Identification Number (EIN) instead of your SSN. It’s a completely separate file from your personal credit report. Having business credit allows your business to borrow money, which is important for growth. Lenders will look at your business credit to get an idea of how reliable you are in paying back loans and decide if they want to work with you. Business credit is essential for things like:- Qualifying for small business loans

- Determining how much credit limit you can get

- Determining business insurance premiums

- Eligibility to open vendor accounts

8 Responsible Ways to Build Business Credit

|

| © CreditDonkey |

What percentage of your total credit do you think you should use?

1. Establish Your Business Formally

Before you can build business credit, you need to establish your business as its own entity separate from yourself. This means you need to register your business as one of the following:- Limited Liability Company (LLC): An LLC limits personal financial liability from the owners while allowing them to record profits and losses on their personal taxes.

- Limited Liability Partnership: This is when two or more partners go into business together. Unlike a normal partnership, you are protected from personal liability.

- Corporation: Corporations are completely independent legal entities that eliminate liability from owners. Because of their tax requirements, however, owners can end up being taxed twice on earnings.

Sole proprietors are not a separate business entity. The proprietor is personally responsible for the business financial obligations. Any profits or losses are recorded on your personal tax returns.

Do I need to get business insurance?

Some businesses are required to get business insurance. If you have employees, for example, you’ll need to provide unemployment, disability, and worker’s compensation insurance. Some states also require additional ones. But required or not, it’s best to get one. It can protect your business from lawsuits, damages, and loss of income.

2. Get an Employer Identification Number (EIN)

An EIN is like a Social Security number for your business. Use it to apply for a business checking account and to file business taxes. To obtain an EIN, you can get one for free on the IRS website. This number is usually issued right away.3. Open a Business Bank Account

A dedicated business banking account is essential to keep a clear divide between your personal and business life. It makes your business more legit and will keep your finances organized. Open the bank account with your business name and EIN. A checking account in itself won’t build business credit. But your banking history is often something lenders look at when you apply for credit. And plus, it helps you establish a relationship with your bank, which can help when you apply for business loans and credit down the road. Here are the best business checking accounts for all types of small businesses.It’s important to separate your business’ expenses from your personal expenses as soon as possible. This article from Lovely Financials explains how to both open a bank account under your business’ name and how to determine if something is business or personal expense.

4. Apply for a DUNS Number

Dun & Bradstreet is the main business credit reporting agency. It’s what most lenders and suppliers use when evaluating your credit. Registering your business with them is one of the first steps to establishing a business credit file. You can register for a DUNS number for free here. If you have had a business credit card or loan before, then you’ll already have a file.5. Get a Dedicated Business Phone Number

Obviously, you need a number for customers, clients, vendors, etc. to call. But that’s not the only reason to get a dedicated phone number just for your business. A business phone number makes your business credible. If you just use your personal mobile number, your business may not seem legit to a lender. You don’t need to buy a new smartphone just to get a business number. You can use a Voice Over IP service (like Grasshopper and RingCentral) to get a business number and forward calls to your current phone.Create Business Social Media Pages

Creating social media pages for your business is another way to connect with your clients. People can reach out to you through them. As small business owners, it also makes your business look professional. LinkedIn, Facebook, and Instagram are popular ones you can use.

6. Establish Trade Credit With Vendors

A lot of vendors and suppliers offer trade credit. This means they first provide the product/service and you don’t have to pay until later. This is essentially like a small loan.For example, Net 30 means you have 30 days to pay after receiving the product. Common terms are 30, 45, 60, 90, or 120 days.

If the vendor reports your payments to the credit bureaus, it will help to build business credit. Ideally, it’s best to confirm if they report before engaging in business.

However, vendors aren’t required to report, so some may not. If yours do not, your business won’t have any record of payment information. If you already have a good relationship with your vendor, you can ask them to report.

Keep in mind that paying early results in a better rating on your business credit report. It’s a useful little bonus that can boost your business.

Ask for Higher Net-30 Credit Line

If you’ve been doing business with the vendor for at least 6 months, you can ask for a higher net-30 credit line. That way, you can keep your credit utilization rate to a minimum.Your credit utilization rate or credit utilization ratio shows how much credit you have used. It’s typically expressed in percent. For example, let’s say you have a $30,000 credit limit and your current balance is $10,000. Your credit utilization rate is 33%.This ratio affects your credit score. It’s best to keep it below 30%.

7. Open a Business Credit Card

Just like banking accounts, you should use a separate credit card just for business. Use your EIN when applying for a business credit card. A business credit card can give you a higher limit, so you have more purchasing power for your business. Another big pro is that a lot of business cards offer business-related rewards and/or an intro 0% APR period. Make sure the business credit card actually will report to the business credit bureaus. And some issuers (such as Capital One and Discover) report to both commercial and personal credit agencies. So having high balances on your business card will also impact your personal credit.8. Get a Business Loan

A lot of growing small businesses need a loan or line or credit at one point or another in order to keep on growing. As you make payments on the loan, they’ll be reported to credit bureaus. You may have to sign a personal guarantee. This is a legal contract saying that you will be personally responsible to repay the loan if your business defaults on the loan. If you have late or non-payments, it could hurt your personal credit as well.Building Business Credit in 30 Days

The fastest way to build good business credit is to start right away. After you’ve formally established your business, consider opening a business credit card or other line of credit.Be sure to pay off your bills on time (or even early) to establish good vendor relationships. And monitor your business credit report regularly for mistakes that may unfairly lower your score.

Benefits of Business Credit

- Lower interest rates A good business credit score will help you gain better interest rates on loans, credit cards, and other lines of credit.

- Eliminate prepay requirements Many suppliers require prepayment if they don’t feel comfortable with your business’ credit history. This can tie up precious cash flow. Having a better credit report can reduce and eliminate the need for prepayment obligations.

- Better trade terms Suppliers can be flexible with their trade terms for the right buyers. A better credit report can give your business leverage when negotiating payment due dates, discounts, and return policies with its suppliers.

- Lower business insurance premiums Insurance companies can look at your credit report to determine your policy rates. A better credit score can get you a lower premium.

- Protect personal credit Using personal credit for business expenses is very risky. It increases your credit utilization ratio and makes your personal credit look bad. Your personal credit will be damaged if you miss business payments or your business fails.Plus, it would make getting loans difficult (both for personal and business) since the two are mixed and lenders can’t get a clear picture. So it’s best to establish separate business credit as soon as possible.

- Easier Expenses Tracking With a business credit card, you can separate your business purchases from your personal expenses. That means you can monitor your business spending more easily. Some business credit cards even provide a breakdown of categories.You can view if your purchase was for a meal, office supplies, etc. Should there be anything suspicious, you can also dispute improper charges.

- Less Time for Tax Report Filing your taxes is less of a hassle since you can deduct business-related purchases more easily. It can also make work more convenient for a certified public accountant (CPA) if you hire one.

Want more info on building business credit? American Business Funders illustrates the different tiers of business credit and what you can expect.

What Are Personal Guarantees?

When you first start your business, you won’t have any business credit. In this case, lenders will usually require a personal guarantee. Personal guarantees essentially require you to act as a co-signer for your business. The same way your children may need you to co-sign on their first car loan, your business needs your support when growing its credit history. As the name suggests, personal guarantees make you personally responsible for the payment of the credit agreement should the business not be able to pay. In other words, signing a personal guarantee can put your personal assets at risk. But they are also an important first step to get your business up and running until it can acquire new lines of credit independently.How the Business Credit Bureaus Work

Much like personal credit bureaus, there are business credit bureaus that collect information about your business activities to provide business credit score and ratings. Here are the 3 major business credit bureaus:Dun and Bradstreet

D&B is the largest business credit agency. It maintains over 300 million company records worldwide. They analyze information provided by businesses and lenders, including payment activity and publicly reported earnings. They generate several different credit scores that lenders may look at, including:[1]- Paydex score: Ranges from 1-100 and evaluates your payment history. This tells lenders and vendors how risky you will be:

- 80-100: always pay on time or early (low risk)

- 50-79: have late payments up to 30 days (moderate risk)

- 0-49: have late payments past 30 days (high risk)

- Failure Score: Indicates how likely the company is to fail within the next year.

- Delinquency Predictor Score (DPS): Indicates risk of delinquency. Ranges from 1-5, with 1 being low risk and 5 being very high risk.

- Supplier Evaluation Risk Rating: Indicates the risk that a supplier will become inactive or shut down in the next 12 months. Ranges from 1 to 9, with 9 being the highest risk.

- D&B Rating: Overall evaluation of a company’s current and future health, and if it will stay in business.

D&B offers a free service, CreditSignal, to help keep your business credit profile on track. Learn more below.

Experian

Experian is a reporting agency for personal credit and also has a small and mid-sized business sector. Their database houses over 99% of all U.S.-based companies. Experian’s business credit score uses a scale of 1 to 100. The higher the score, the lower your risk to lenders.[2]- 76 – 100: Low Risk

- 51 – 75: Low to Medium Risk

- 26 – 50: Medium Risk

- 11 – 25: High to Medium Risk

- 0 – 10: High Risk

- Payment habits

- Outstanding balances

- Number of trade experiences

- Credit utilization

- Trends over time

- Company background info, public records, and legal filings

Equifax

Equifax also reports on business credit, including payment history, bankruptcies, public records, and business demographics. It generates 3 business credit scores:[3]- Business Payment Index: Evaluates your payment history in the past year. Ranges from 1-100. A score of 90-100 means that you always pay your bills on time. 80 means you had at least one late payment.

- Business Credit Risk Score: Indicates how likely it is for you to make late payments. It’s graded on a scale of 101 – 992. The higher the score, the less risk. A score of 700 or higher is considered good.

- Business Failure Score: Indicates the likelihood of failure within the next 12 months. Ranges from 1000 – 1880, with higher scores suggesting less risk.

How to Maintain Good Business Credit

After you’ve established some business credit, it’s important to maintain it. Here are some tips to maintain or improve your business credit:- Pay bills on time. This is perhaps the most important thing you can do. Your payment history tells lenders how much debt-risk you carry.

- Lower your credit card utilization ratio. In other words, don’t max out your business credit cards. If you need more credit, it may be better to open a small business loan instead.

- Make sure your suppliers report: Even if you have good relationships with your suppliers, it’s no use if they don’t report to the business bureaus. It’s best to only work with suppliers that do report. If your supplier does not, you can manually submit trade references.

- Update your business information: If you have info that’s out of date, that could affect you getting a loan or setting up trade credit. Keep your info updated with the DUNS manager tool.

- Dispute errors. See a negative remark that you believe to be inaccurate? You can dispute it with the business that made the report, or directly with the bureau. Your dispute will be investigated and removed from your credit report if you can prove your case.

If you really have missed payments with creditors, you can negotiate with them. You can offer to pay the account in full, and in exchange, they remove the negative remarks off your credit report.

Monitoring Business Credit

It’s also equally important to regularly monitor your business credit to make sure it’s accurate. Unlike consumers, businesses are not legally entitled to a free credit report. Most business credit reports will cost you. Read on to learn about CreditSignal, one of the best free options.Mistakes can be costly. Lenders use credit reports to determine payment terms and interest rates. Having incorrect information on your business’ credit report can seriously impact cash flow.

CreditSignal (free)

CreditSignal is a free service provided by Dun and Bradstreet. It alerts you to changes to your D&B Paydex, Delinquency Predictor Score, Financial Stress Score, and Supplier Evaluation Risk rating.

One downside: CreditSignal only provides information from their platform. However, D&B is one of the largest business credit reporting agencies. So this is a great way to start monitoring your business credit.

Paid Options

Outside of CreditSignal, your best bet is to pay for a full credit report. Doing so will give you the best picture of your business’ financial health.

D&B, Equifax, and Experian all offer paid subscription services that allow you to monitor your business credit report.

You can also purchase one-time credit reports through Equifax and Experian. These can be more cost effective for your growing business—as long as you remember to monitor them regularly.

Starting a business with bad personal credit

You can build strong business credit even with poor personal credit. But you may need to get creative when applying for financing since lenders will likely review your personal finances until your company develops its own credit profile. Start by formally establishing your business. Then look into financing options like:- Trade credit

- Secured business credit cards

- Revenue-based financing

Frequently Asked Questions

What types of business entities have business credit? Types of business entities include sole proprietorships, partnerships, LLCs, and corporations. And you can establish business credit regardless of the type of entity your company is. You can apply for business credit cards or use other types of credit such as vendor credit or retail credit. How do I build business credit fast? To build business credit fast, make sure you’ve set up the right business structure. Then, register with a credit agency such as Experian, and work with vendors who report your transactions. Make sure to pay your bills on time and limit your credit use to 30% of your limit. This helps avoid negative impacts on your score. Can a personal credit card help build business credit? Business credit can affect personal credit but not the other way around. That means you can’t use your personal credit to build your business credit. Consumer credit bureaus will not report to business credit bureaus. But the latter will report to the former some activities such as defaults. How long does it take to build business credit? There’s no specific length of time for you to build business credit. But generally, 1-3 years is a good rule of thumb. You’ll want to ensure your business has solid financial health within this period. And you’ll want to make on-time payments to show that you can handle debt responsibly. Do all of my accounts appear on my business credit reports? Not all of your accounts might appear on your business credit reports. That’s because businesses you work with aren’t required to report your activities. If a vendor, for example, doesn’t report to a credit bureau, then your credit score won’t be impacted even if you pay them in a timely manner. How can I add an account that I already have to my business credit reports? You can’t add account transactions to your business credit reports. Only the businesses or vendors you work with can report on your behalf. Keep in mind that they’re not required to report to credit bureaus, so you may have to ask them to.What the Experts Say

CreditDonkey asked industry experts to answer readers’ most pressing questions about building credit safely. Here’s what they said:Bottom Line

Building business credit doesn’t have to be a daunting process. Establish the separation between your business and personal finances right away. Take out small lines of credit using a personal guarantee so that your business can get approved for larger projects later. Then monitor your business credit profile and consistently update information as needed. Follow these steps to give your business a healthy credit start.References

- ^ Dun & Bradstreet Business Credit Scores & Ratings, Retrieved 1/9/2022

- ^ Experian Credit Ranking Score, Retrieved 1/9/2022

- ^ Equifax Business Credit Reports, Retrieved 1/9/2022

How to Get a Business Credit Card

Read more about Business

Editorial Note: This content is not provided by the card issuer. Opinions expressed here are author’s alone, not those of the issuer, and have not been reviewed, approved or otherwise endorsed by the issuer.

Ad Disclosure: This article contains references to products from our partners. We receive compensation if you apply or shop through links in our content. This compensation may impact how and where products appear on this site. You help support CreditDonkey by using our links. (read more)

Applying for a business credit card is easier than it sounds. Here is how to apply for one, whether you have a corporation or a freelance side hustle.

A business credit card is a great way to get extra rewards and perks.

But not all cards are created equal.

Read on for everything to know about how to apply for a business credit card.

For new businesses and first-time applicants, here are some things to know about getting approved.

Every business credit card is different and there are some better suited for certain types of entrepreneurs than others. When you’re shopping around for a card, keep your eyes on these four things:

Rebecca Lake is a journalist at CreditDonkey, a credit card comparison and reviews website. Write to Rebecca Lake at rebecca@creditdonkey.com. Follow us on Twitter and Facebook for our latest posts.

Note: This website is made possible through financial relationships with some of the products and services mentioned on this site. We may receive compensation if you shop through links in our content. You do not have to use our links, but you help support CreditDonkey if you do.

Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. This site may be compensated through the Advertiser’s affiliate programs.

Editorial Note: This content is not provided by Chase. Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Chase. This site may be compensated through the Advertiser’s affiliate programs.

Read Next:

|

- Who Can Apply?

- What You Need to Apply

- Getting Approved

- How to Compare Cards

- Frequently Asked Questions

Here are 5 steps to qualify for a business credit card:

- Have a small business with the intent to make a profit.

- Know your credit score so you know which cards you qualify for.

- Compare business credit card offers to find the best one for you.

- Fill out application with your business name and EIN (or your name and SSN).

- Wait for approval. Or call for reconsideration if rejected.

Tip: As a small business owner, you know that credit cards can be a lifesaver. But it’s not always easy to know where to start when it comes to applying for a business credit card. You’ve probably heard that getting a business credit card is important, but you don’t want to get taken advantage of by high interest rates or unfair fees.

Consider this: Ink Business Cash lets you earn $350 when you spend $3,000 on purchases in the first three months and an additional $400 when you spend $6,000 on purchases in the first six months after account opening. Earn 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet, cable and phone services each account anniversary year. Earn 2% cash back on the first $25,000 spent in combined purchases at gas stations and restaurants each account anniversary year. Earn 1% cash back on all other card purchases. There is no annual fee.

Plus, there is a 0% introductory APR on purchases for 12 months. After the intro period, a variable APR applies, currently 17.99% – 25.99%.

Who Can Apply?

Business cards aren’t just for corporations. You can apply for a business card even if you’re running a one-man show and have no office. You may be surprised by what could be considered a business. Here are just some examples:- If you’re a freelance web designer

- If you have an Etsy shop

- If you sell books on Ebay

- If you drive Uber in your spare time

- If you tutor students

- If you sell cookies at the farmer’s market

- Keep your business expenses separated. This will make it so much easier come tax time.

- Earn rewards in business categories. Besides the tempting bonuses, business credit cards generally give bonus cash back or points in popular business categories (such as office supply stores, advertising online, telecommunication services, etc.)

Ink Business Cash® Credit Card

Earn 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet, cable and phone services each account anniversary year. Earn 2% cash back on the first $25,000 spent in combined purchases at gas stations and restaurants each account anniversary year. Earn 1% cash back on all other purchases. - More purchasing power. Having a separate business credit card will mean that you have more credit for business expenses. Also, business credit cards tend to give higher credit lines than personal cards.

What You Need to Apply

Here comes the fun part: Applying for a business credit card when you’re just starting out can make you feel more official. It’s a little different than applying for a personal credit card. Here’s a rundown of how to fill out the application:- The business’ legal name

This is the name you use to do business. It’s what will show up on your card if you’re approved.If you have a corporation or an LLC, enter the business name that you registered with your state government.If you’re a freelancer or sole proprietor, just use your legal name on this line.

Tip: Small business can also file a “Doing Business As” or DBA. This allows you to operate under another business name (instead of your own name). If you have done this, apply with your DBA name.

- Your tax identification number You’ll need a tax identification number to process your application.Incorporated businesses and partnerships enter their federal Employer Identification Number. This is a nine-digit number issued by the IRS for tax reporting purposes.If you’re a freelancer, you’d enter your Social Security number on this line (unless you have an IRS-issued Employer Identification Number).

- The business type or business structure

This is the kind of business you’re operating. If you’re an LLC, you’d choose partnership or corporation, based on how it’s set up. If you are a freelancer, you would usually put down sole proprietorship.

Beneficial owners: Effective May 11, 2018, new regulations require that important personal information is also provided for beneficial owners. This is anyone who directly or indirectly owns 25 percent or more of the business. This includes names, birth dates, social security numbers, home addresses and percent of ownership. Their credit information is not pulled, but records are kept for informational purposes.[1]

- The industry type or nature of the business

Credit card companies also want to know what kind of business you’re running. You’ll have a list of industries to choose from. Just select the one that fits best, even if it isn’t quite the exact label.

Related: Successful People Do These 23 Things Daily

- Your role in the business

Spell out what you do. For example, you can say you’re the owner, president, or general manager.

Related: CEO Statistics

- Business address and phone number You’ll need to fill in the contact information for your business. If you run your business from home, just use your home address here.

- How long you’ve been in business

Enter the number of years you’ve been in business. If you’re still in the early startup phase, just enter “0” in this box.

Related: Startup Failure Rate Statistics

- The number of employees Enter the number of employees you have, if any. If it’s just you, enter “1” for yourself.

- Annual business revenue

You have to let the credit card company in on how much revenue your business is bringing in each year. If your business is new and you haven’t made a buck yet, it’s fine to put “0.”

Related: How to Make Customers Happy

- Estimated monthly spend

This just means your most accurate guess of what you think you’ll charge to the card each month. Not all business card applications ask for this, but you should be ready with an answer if it comes up. Make sure this is what you will charge for business expenses, not personal.Aside from your business information, you’ll need to connect the dots on your own personal details. That means filling in:

- Your name

- Address, phone number and email

- Social Security number

- Birth date

- Mother’s maiden name

- Household income

Getting Approved for a Business Credit Card

|

Earn $350 when you spend $3,000 on purchases in the first three months and an additional $400 when you spend $6,000 on purchases in the first six months after account opening

- It is dependent on your personal credit. Since you don’t have any business history yet, the banks will look at your personal credit history and score. The better your personal credit score is, the easier it is to qualify.

What’s your credit score?That won’t come into play as much for an established business, since you would have a separate business credit history built up.Getting a business card with bad credit: Owners with low (or no) credit can still get a business credit card but options are limited. Companies like Capital One offer cards to people with lower credit scores. They will check your personal credit score, however. You might also consider a secured credit card. These cards have lower credit requirements but require a deposit in case you default on payments. A prepaid card is a viable option and doesn’t require a credit score check, but it does not help you build credit.

- You probably need to sign a personal guarantee. This is a clause that states you’re personally responsible for the repayment of business debt. Banks often need this assurance that someone will be responsible. If you stop making payments on the card because the business fails, the bank can come after you personally to recover the balance owed.

- Do not lie on the application. Even if you need to put “0” as the revenue, it’s better to do that than lie. You may get a phone call asking for more information. Be prepared for questions about the nature of your business and how much you expect to make.Just tell the truth that you’re in the startup phase. Explain why you want the business card now. For example, maybe the reward structure will really help you, and you want to keep expenses separate.

- A relationship with the bank helps. If you’re already a customer with the bank and your accounts are in good standing, it may make it easier to apply for a business card with the same bank.

How do you obtain business credit? Here are simple steps to build business credit history:

- Form an LLC or incorporate to help separate your personal credit from that of your company.

- Apply for an EIN number. (This number will represent your business in tax filings and legal documents).

- Start a business bank account. Make sure to keep your personal financial business separate from this account.

- Apply for a business credit card. This will help you grow a line of credit for your new company.

- Pay all bills and invoices on time to build your credit history and reputation with vendors.

How to Compare Cards

|

- APR: The APR, or annual percentage rate, determines the amount of interest you’ll pay over the course of a year if you carry a balance. Many business cards offer a 0% introductory rate on purchases for new card members, which can give your new business some breathing room.

- Fees: Scoring a card with a low APR isn’t such a sweet deal if it comes with lots of fees. If your goal is earning rewards, for example, make sure they’re not being wiped out by a high annual fee. If you travel, steer clear of cards that charge a foreign transaction fee. This fee can add up to 3% to the cost of purchases made abroad.

- Rewards: Earning big rewards is one of the best reasons to get a business credit card. Choose a card with a rewards structure that aligns with your business expenses. Think about whether you want points, miles or cash back; and whether you want bonus categories or a flat rate per dollar. Also, consider your redemption options. If you’re after a big bonus, make sure you can meet the minimum spending requirement.

What is the best small business credit card? Ink Business Preferred lets you earn 90k bonus points after you spend $8,000 on purchases in the first 3 months from account opening. That’s $900 cash back or $1,125 toward travel when redeemed through Chase Travel℠. Earn 3 points per $1 on the first $150,000 spent in combined purchases on travel, shipping purchases, Internet, cable and phone services, advertising purchases made with social media sites and search engines each account anniversary year. Earn 1 point per $1 on all other purchases. There are no foreign transaction fees. There is a $95 annual fee.

- Card type: Business credit cards will allow you to carry a balance, but charge cards require you to pay in full each month. Charge cards don’t charge interest but there’s no flexibility if you need to pay just the minimum one month. If you don’t have a steady cash flow, you need to have a revolving credit card account instead.

Frequently Asked Questions

- Can I apply for business credit card even if I’m not yet earning income? Yes. You can apply as long as you have a reasonable intention to make a profit.

- I really like the rewards on a certain business card. Can I use it for personal expenses too?

We advise that you don’t mix personal and business expenses. It’ll cause more headache when you need to separate out your business expenses when filing taxes.And if you fall behind on your payments, the card issuer may look at your activities more closely. If they see that there are personal expenses on there, you may lose your rewards and your account could be closed or changed to a personal card.

Note: If you operate as an LLC, corporation, or partnership, then it’s even more important to keep your business separate from your personal life. At this point, there are legal considerations too. If you mix personal and business spending on a credit card, then the business and the person can be seen as the same. That may expose you to additional liabilities.

- Do I have to also have a business checking account in order to have a business credit card? If you’re an independent freelancer or have other small jobs (in other words, if you’re a sole proprietor), then no, you do not usually need to have a business checking account.If you have formed an LLC, partnership, or DBA (Doing Business As), then you do need a separate business banking account. These kinds of business require that you separate business and personal finances.

- Will a business credit card affect my personal credit? Generally, business credit cards don’t report to personal credit bureaus. So your personal credit won’t be impacted if you have high business expenses. However, if you keep on making late payments or missing them, then your personal credit may take a ding.

What the Experts Say

CreditDonkey asked a panel of industry experts to answer readers’ most pressing questions. Here’s what they said:Bottom Line

In short, you can apply for a business card as long as you are earning profit (or intend to). There are plenty of incentives for choosing a business credit card over a personal credit card. You can keep your personal and business expenses separate, and you may be able to get higher rewards for your business-related charges. However, once you get it, use the card responsibly and abide by the cardholder agreement.

|

|||||||||||||||

References

- ^ FinCEN.gov. Information on Complying with the Customer Due Diligence (CDD) Final Rule, Retrieved 11/28/2022

Pingback: Best Credit Card Reader for iPhone - Creditofferly